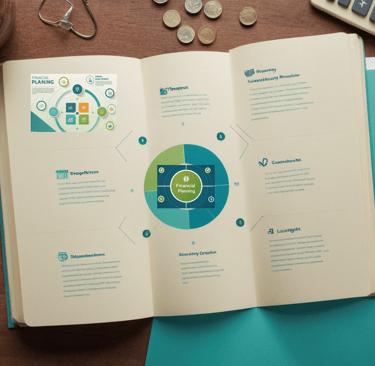

Financial Planning Process: 5 Key Steps to Building Financial Security

This blog covers the 5 essential steps to effective financial planning, from setting goals to monitoring progress, helping you build a secure financial future with confidence. Follow these actionable steps to take control of your finances and achieve long-term stability.

FINANCIAL PLANNING

Do you feel uncertain about where your finances are headed? Many people seek financial security but are unsure how to achieve it with so many options and decisions to make. Financial planning is essential in creating a structured approach to reaching your goals, helping you build confidence and peace of mind. This guide walks through the 5 essential steps in the financial planning process, designed to help you take control of your financial future and reach meaningful milestones.

Financial planning begins with a clear set of goals. Without defining your objectives, it’s difficult to know what financial security truly looks like for you. This step isn’t just about setting goals but also understanding what success means on a personal level, whether it’s a secure retirement, buying a home, or funding your child’s education.

Short-Term vs. Long-Term Goals: Categorize your goals by timeframe. Short-term goals might include paying off credit card debt or building an emergency fund, while long-term goals might be buying a home or building retirement savings.

SMART Goals: Make your goals Specific, Measurable, Achievable, Relevant, and Time-bound. This structure makes it easier to monitor progress.

Example: Instead of “I want to save more,” define it as “I want to save $10,000 for a home down payment in the next 3 years.”

Prioritize Goals: Determine which goals are most important to you. By assigning priorities, you can allocate resources effectively without feeling overwhelmed.

Set Milestones: Break down big goals into smaller, achievable steps. For example, if your goal is to save $100,000 for retirement, aim for smaller milestones, like saving $5,000 by year one, $25,000 by year five, etc.

1. Setting Clear Financial Goals

2. Gathering Financial Information

A successful financial plan requires a full understanding of your current financial situation, a process often called “fact-finding.”

Income Sources: List all income sources, including salary, freelance work, and passive income, to gauge your financial base. Knowing where your income comes from and how stable it is helps in setting realistic goals.

Tracking Expenses and Cash Flow: Track both fixed and variable expenses to get a clear view of your monthly spending. Use a budgeting app or spreadsheet to categorize your expenses:

Fixed: Rent, utilities, loan payments.

Variable: Groceries, gas, entertainment.

Discretionary: Dining out, hobbies.

Assessing Assets and Liabilities: List assets (savings, investments, property) and liabilities (debts, loans). Calculate your net worth by subtracting liabilities from assets to get an overview of your financial health.

Organizing Financial Documents: Gather essential documents like bank statements, tax returns, and investment records. This makes planning easier and ensures you don’t miss critical details.

3. Developing a Customized Financial Plan

A customized financial plan aligns your spending, saving, and investing with your goals and lifestyle.

Budgeting and Saving: Establish a budget to control spending and allocate funds to savings. Use the 50/30/20 rule as a starting point: 50% of income goes to needs, 30% to wants, and 20% to savings or debt repayment.

Investment Strategy: Decide on an investment approach based on your risk tolerance and time horizon.

High Growth: Stocks, ideal for long-term growth but higher risk.

Stability: Bonds offer steady returns and are lower-risk.

Diversification: ETFs or mutual funds provide a balanced approach, diversifying investments across multiple assets.

Debt Reduction: Create a structured plan to reduce high-interest debt, prioritizing payments on credit cards or loans.

Insurance and Risk Management: Evaluate insurance needs (health, life, property) to protect against unexpected events that could disrupt your plan.

With a solid plan in place, it’s time to take action. Implementing your financial plan is a gradual process that requires consistency and patience.

Automate Savings and Investments: Set up automatic transfers to savings or investment accounts. This “pay-yourself-first” approach ensures consistent progress without effort.

Build an Emergency Fund: Aim to save 3-6 months’ worth of expenses in an easily accessible account to cover unexpected costs.

Allocate Resources Based on Priorities: Focus on funding high-priority goals first, like building an emergency fund or repaying high-interest debt.

Track Progress Regularly: Schedule quarterly reviews to adjust your budget and contributions as needed. Life changes, income fluctuations, or shifting priorities may require plan adjustments.

4. Implementing the Financial Plan

5. Monitoring and Adjusting the Plan Over Time

A financial plan isn’t a “set it and forget it” process; it requires periodic adjustments as life changes and new opportunities arise.

Stay Updated on Market and Economic Changes: Market shifts can impact your portfolio. Stay informed about economic trends and consider adjusting your investments when necessary.

Adapting to Life Events: Major life changes, like a job shift, marriage, or a new addition to the family, can impact your goals and resources. Adjust your plan as these events unfold.

Schedule Annual Financial Check-Ups: Set aside time once a year to review income, expenses, and investment performance.

Exploring New Opportunities: Stay open to emerging investment options, such as sustainable funds or real estate opportunities, that could enhance your financial plan.

Set New Milestones: Regularly update your goals to reflect your progress and new financial aspirations.

Financial planning is an ongoing process that adapts with your life and goals. By regularly monitoring and adjusting your plan, you’ll stay on track to build a secure, resilient financial future. With these 5 key steps, you can navigate financial challenges confidently and move closer to achieving the peace of mind that comes with financial security.

About us

Quick links

Services

Follow us

SVM Business excel at providing comprehensive financial solutions that empower clients to achieve their ambitions. With expertise in Investment Management, Insurance Solutions, Financing Solutions, Capital Market Operations and Currency & Commodity SVM offers tailored services across strategies, planning, management and more.

Privacy | Refund | Disclaimer

Powered by SVM Business